Solutions to Assignments

MMPC - 004 - Accounting for Managers

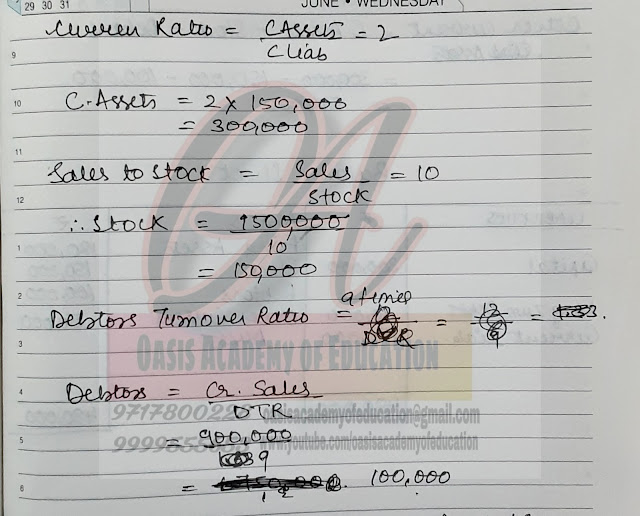

Solutions to Question No. 5

If you turn on the news today, you will likely see a story related to fraudulent activity. As criminals and scammers adapt to a world that revolves around the internet, committing fraud has become far easier. According to the Global Fraud and Identity Report, 33% of businesses experienced more fraud losses than they did in the prior year. Thankfully, people with excellent numerical skills are seeking employment as forensic accountants. Forensic accountants use their auditing abilities combined with investigative skills to determine what causes suspicious financial activity. Businesses use this information as credible evidence in trials and/or to recover losses from a scam.

Forensic accounting is the term used to describe the type of engagement. It is the whole process of carrying out a forensic investigation, including preparing an expert’s report or witness statement, and potentially acting as an expert witness in legal proceedings.

Forensic investigation is a part of a forensic accounting engagement. Forensic investigation is the process of gathering evidence so that the expert’s report or witness statement can be prepared. It includes forensic auditing, but incorporates a much broader range of investigative techniques, such as interviewing witnesses and suspects, imaging or recovering computer files including emails, physical searches of premises etc.

Forensic auditing is the application of traditional auditing procedures and techniques in order to gather evidence as part of the forensic investigation.

- Method of Fraud Detection in Forensic Audit

The major applications of forensic accounting include fraud investigations, negligence cases and insurance claims.

An insurance claim would require determination of how much the client should claim from the insurer. The first step would be a detailed review of the insurance policy to determine ‘coverage’, ie what is insured and any clauses that might restrict the amount that can be claimed or invalidate the claim.

The second step would be to gather evidence to quantify the loss, ie the amount to be claimed. Insurance claims might include claims following misappropriation of assets, ie theft of goods or money. In such cases, the forensic accountant will review inventory or cash records and details of sales and purchases to reconcile the amounts held and determine the value of the goods or cash stolen. They will also test the reliability of the information held by counting a sample of inventory or cash currently held in comparison with the client’s records. The forensic accountant will not assume that there has been a theft; they will consider other possibilities such as an error in the data held.

Insurance claims may however, be much more complicated than this, such as in the case of business interruptions arising as a result of fire or flood. In these types of engagements the forensic accountant will review prospective financial information in comparison with reported outturn to evaluate the loss of profit arising as a result of the business interruption. The forensic accountant will not assume that there has been any loss of profit due to the business interruption; they will consider other possibilities such as a straightforward loss of market share to a competitor.

Forensic engagements often require the forensic accountant to quantify a loss. One such engagement is in professional negligence claims, ie when another accountant has breached their duty of care to a client or third party resulting in a loss for that client. In these types of engagement, the forensic accountant would also provide an opinion on whether the duty of care owed has been breached, ie whether the audit or other accountancy service was performed in accordance with current standards in practice, legislation and techniques. In relation to an audit, this would require consideration of whether the International Standards on Auditing were followed.

The need for a forensic accountant may also arise because two parties cannot agree on the amount owed by one party to another, and the accountant is engaged to provide an expert valuation, of a business for example.

This might be the case in a matrimonial dispute, where a divorcing couple whose assets include shares in a company or partnership, engage a forensic accountant to value the company so that a settlement can be reached. A similar process might apply in partnerships, when one partner wishes to leave the partnership and is being bought out by the remaining partner(s).

- Techniques in Forensic Audit

There are several techniques for conducting a forensic review of the business. The ones provided below are generic but effective. These are the forensic techniques that apply to almost all companies. These are:

1. Reviewing Public Documents and Conducting Background Checks

The documents made available to the public are scrutinized as they are the easiest to obtain. Also, thorough background checks of a particular company are done to see the past dealings of the business. Public Documents would include any information in the public database, the corporate records, and any legally available information on the internet.

2. Conducting Detailed Interviews

Conducting an interview is an essential technique that can transform an unwilling person into a source of valuable information. It helps in fully understanding all the facts. An interview should be conducted by accurately assessing the gravity of the situation and preparing the questions according to it. Discussions should take every detail into account and look at the greater picture to figure out the magnitude of the illegal activity and the culprit responsible.

3. Gathering Information from Trustworthy Sources

Information provided by a confidential and trustworthy source can be precious to any case. When a piece of information is gained from a confidential source or a confidential informant, all the necessary precautions should be taken to hide the identity of the so-called cause. A forensic accountant should try to have as many confidential sources as possible because such sources can virtually guarantee a correct result.

4. Analyzing Evidence Gathered

Proper analysis of the obtained evidence can point to the guilty party and assist in understanding the extent of the fraud committed in the business. Furthermore, this analysis would also help understand how secure the company is against financial scams and installing various austerity measures to prevent any such future situation.

5. Conducting Surveillance

This can be done physically or electronically and is one of the conventional measures to uncover any fraud. It can be done by monitoring and tracking all the official emails and messages.

6. Going Undercover

This is an extreme measure and should be used only as a last resort. It is best left to the professionals as they know how and where to conduct the investigations. Even a small mistake while being undercover can signal the offender that something is wrong, and the person might vanish.

7. Analyzing the Financial Statements

This is a special tool for finding out the fraud committed. All the necessary details are summarised in the financial statement, and the analysis of these statements can help a forensic accountant figure out the scam.

Nowadays, the economic conditions are getting stricter, and each country’s government is now implementing tighter laws regarding the governance of the businesses. As the companies are increasing the level of sophistication, so is fraud. This has led to a higher sensitivity to fraud which can be interpreted as massive demand for the services of forensic accountants by all the businesses.