Solutions to Assignments

MMPC - 004 - Accounting for Managers

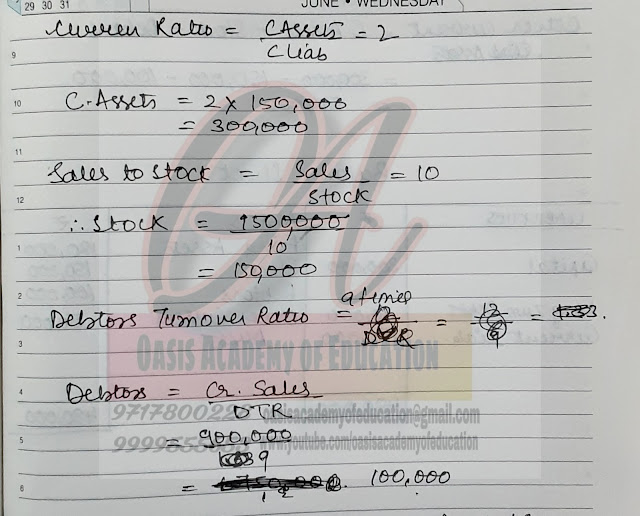

Solutions to Question No. 3

Need and Importance of Variance Control

1. Acts As A Monitoring And Control Tool

Technically, variance analysis isn’t a monitoring tool. Instead, forecasts and budgets provide a basis for analyzing costs. However, companies cannot actually monitor their costs if they don’t compare them with actual results. It is where variance analysis is helpful. Companies can use variance analysis to calculate any differences between budgets and actual results. Through this process, companies can actively identify any efficiencies and eliminate them on time. This way, companies can control any deviations from the set plans for performance. Similarly, companies can also accumulate all the information and perform variance analysis at the end of each period. Based on this process, they can make changes that can help avoid any inefficiencies in the future.

2. Focuses On Favourable And Adverse Variances

Unlike some other tools, variance analysis focuses on both favorable and adverse variances. Although favorable variances are beneficial for companies, they still need to the reason behind it. Sometimes, these variances may come from miscalculations or improper budgeting, which companies should investigate. If that is not the case, companies still need to understand how these variances generated so they can build on the favorable performance. Adverse variances, on the other hand, are harmful to the company. By analyzing these, companies can identify problem areas within their processes. By doing so, they can eliminate any problems which can be beneficial in the future. Some companies may only focus on adverse variances, though. However, variance analysis provides a tool to identify both favorable and adverse variances.

3. Considers Significant Variances

Variance analysis is a great tool to catch and rectify significant variances. Companies can suffer variances in actual performance due to several reasons. Sometimes, these reasons may be random or seasonal. However, variance analysis allows companies to adjust for these variances and allows a better performance analysis. Similarly, variance analysis allows companies to consider material variances only. During the process, companies can set a threshold for the difference that they want to investigate. If any variance does not meet this threshold, companies can ignore that. This way, the process is much straightforward.

4. Detects Inefficiencies In Planning Or Operations

Variance analysis takes a budget and compares actual performances with it. However, it doesn’t focus on operational inefficiencies only. It also allows companies to examine their budgets for any unrealistic expectations. This way, companies can identify any problems with their forecasts and rectify them for the future. Most of the time, however, variance analysis catches operational inefficiencies. It is one of the reasons why companies use it. Operational anomalies are common in every business environment. By identifying these, companies can uncover any problematic areas within their process and correct any errors.

5. Provides A Basis For Accountability

As mentioned, companies may focus on variance analysis toward specific areas. This way, variance analysis can allow companies to hold their managers accountable for their performance. Furthermore, companies can differentiate between controllable and uncontrollable variance. Through this process, they can further identify the departments or managers responsible for variances. Some companies may also use variance analysis as a part of their performance appraisal. Similarly, companies may also reward managers for favorable variances. This way, variance analysis can provide an accountability tool for companies. Likewise, if the expectations are reasonable, companies can use variance analysis as a motivation tool.